2025-05-05

Incorrect VAT Rate on Your Purchase Invoice?

Incorrect VAT Rate on Your Purchase Invoice? You May Still Deduct It – Even If the Seller Applied the Wrong Amount. The Polish tax authorities confirm that an incorrect VAT rate shown on a supplier’s invoice does not automatically disqualify the purchaser from deducting input VAT – provided that all other legal conditions for deduction are fulfilled. A recent example is the individual tax ruling issued on Nov. 15, 2024 (case: https://lnkd.in/d2htU_aF). An even more recent example (ruling in case 0112-KDIL1-3.4012.556.2023.2.KK) proves that the right to deduct input VAT may still apply even if the purchased goods or services should have been taxed at the 0% (preferential) rate yet were incorrectly charged at 23%.

Incorrect VAT Rate on Your Purchase Invoice? You May Still Deduct It – Even If the Seller Applied the Wrong Amount.

The Polish tax authorities confirm that an incorrect VAT rate shown on a supplier’s invoice does not automatically disqualify the purchaser from deducting input VAT – provided that all other legal conditions for deduction are fulfilled. A recent example is the individual tax ruling issued on Nov. 15, 2024 (case: https://lnkd.in/d2htU_aF). An even more recent example (ruling in case 0112-KDIL1-3.4012.556.2023.2.KK) proves that the right to deduct input VAT may still apply even if the purchased goods or services should have been taxed at the 0% (preferential) rate yet were incorrectly charged at 23%.

Legal Background:

Under Polish VAT law (Art. 88 of the VAT-Act), certain cases where input VAT deduction is restricted are listed exhaustively. They do not include a scenario where the supplier applied an incorrect VAT rate on the invoice (e.g. 23% instead of 8%).

This confirms a long-standing principle of EU VAT law: deduction rights are fundamental to ensuring VAT neutrality and cannot be limited without clear legislative basis.

Practical Implication for Your Business:

Both local and cross-border transactions might lead to misunderstandings in VAT rates – especially in sectors like logistics, construction, or digital services. Those rulings provide a degree of legal certainty for businesses operating in Poland:

If the purchase is linked to Your taxable activities,

the purchased goods/services were neither VAT-exempt nor subject to specific “standstill” regulations (like ban on VAT deduction on purchased accommodation or restaurant services), and

The invoice contains required formal elements,

the buyer retains the right to deduct input VAT, even if the VAT rate was incorrect.

How can you protect your business?

Verify the substance over form: focus on the nature of the transaction, not just the invoice layout.

Ensure your purchases are properly linked to VAT-taxable sales.

Don’t rush to self-assess the amount of deductible VAT – consult a tax advisor first.

Our team advises international companies on navigating VAT compliance in Poland and across the EU.

Reach out if your business faces issues with invoice corrections, tax audits, or intra-EU transactions.

See other articles

The general tax ruling issued by the Polish Minister of Finance and Economy on 27th of November 2025 addresses the issue of land, buildings and structures being deemed as “related to business activity”. It is one of the most significant documents in recent years in the area of property taxation. Its importance goes well beyond a purely technical explanation of statutory provisions. At its core, it touches on a fundamental and long-running dispute between taxpayers and tax authorities: where the line should be drawn between mere ownership of real estate and its use for business purposes.

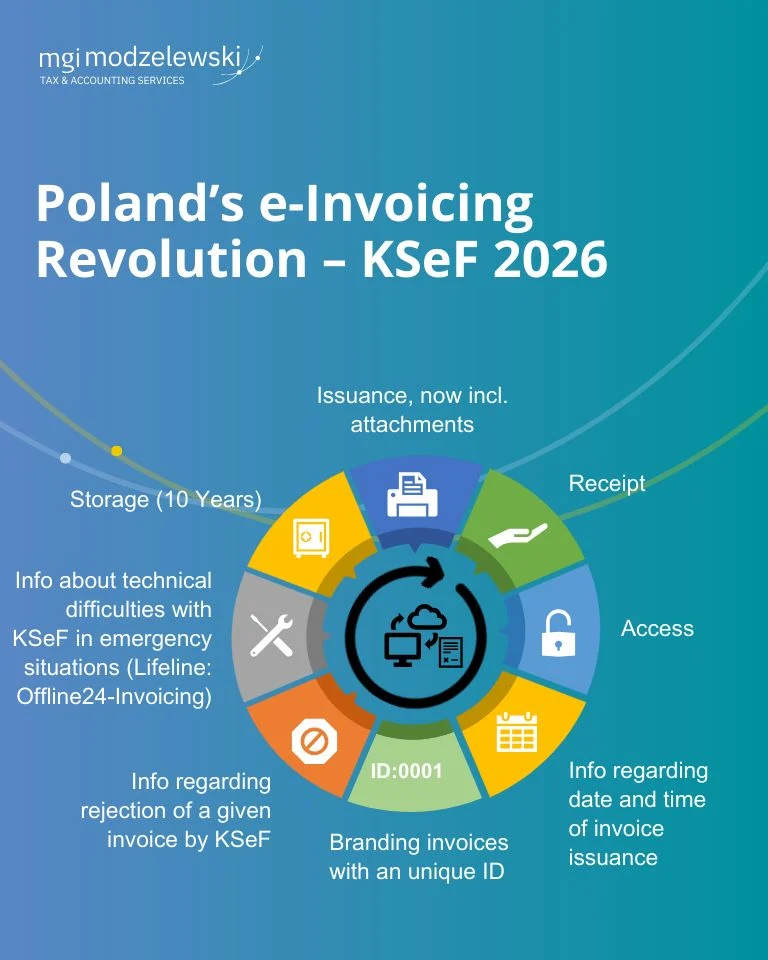

Even though penalties for issuing invoices outside Poland’s National e-Invoicing System (KSeF) have been deferred until 1 January 2027, the real headache may come sooner.

The Court held that, in certain circumstances, contractual penalties for delays may qualify as tax-deductible in Polish CIT. The case concerned a property developer unable to hand over apartments to clients in time, due to delays caused by the general contractor. The clients charged contractual penalties, which the developer has paid and qualified as tax-deductible costs. The Polish tax authority (KIS) argued that any penalty for non-performance or improper performance is excluded from tax costs under Art. 16(1)(22) of the Polish CIT Act. The Polish Supreme Administrative Court (NSA) disagreed.

CJEU: Is a TP profit true-up a service? Key takeaways from 4 Sep 2025 (C-726/23, Arcomet) The Court held that intra-group payments determined under TNMM (e.g., skimming part of a subsidiary’s operating margin above a threshold) can be deemed as consideration for services and thus fall within VAT—if there is a legal relationship and a direct link between the supply and the consideration.

Is a plot of land with a building scheduled for demolition considered ‘undeveloped land’? Under the Polish VAT Act, the sale of undeveloped land is exempt from VAT as long as it does not have the status of ‘building land’. Otherwise, such sale might be subject to 23% VAT. In contrast, the VAT on a sale of a developed plot of land is determined based on the history of the buildings/structures. In general: older buildings = VAT-exemption. A recurring question, however, is how to classify land where there are buildings or structures in poor condition that are intended to be demolished. Can such a property still be treated as “developed” for VAT purposes? The question might seem irrelevant, yet there is another layer to it. According to Polish tax law, if the sale of immovable property (plot, building) is not subject to VAT at all or is VAT-exempt, the buyer must pay a 2% tax on civil law transactions (Podatek od czynnosci cywilnoprawnych, also known as PCC). Thus, many B2B-sales aim at having the transaction taxed with VAT (deductible) to avoid PCC (non-deductible).

KSeF 2.0 is here – the President of Poland has signed the bill! On August 27, 2025, the President approved amendments to the VAT Act introducing the new version of the National e-Invoicing System (KSeF). This marks one of the most significant tax reforms in recent years – transforming how every Polish company or entrepreneur issues and processes invoices.

Advance invoices issued too early – a key change in Polish VAT practice On 23 July 2025, the Polish tax administration has published (ref. DOP7.8101.28.2025.FMLM) a revision to a ruling issued in 2017 which reshapes the treatment of prematurely issued advance invoices. Previous approach Article 106i(7) of the Polish VAT Act allows most invoices (with limited exceptions) to be issued up to 60 days before supply, performance of a service or receipt of an advance payment. Prior to 2022, the limit was 30 days, whereas before 2014 such an option did not exist at all. Those changes were welcomed by many firms, as some B2B clients (particularly larger companies in the construction sector) requested advance invoices even weeks before contractual payment dates. In other words: for some firms it was/is a “must have”.

Employee wellbeing and taxes — do wellness benefits create taxable income? In today’s workplace, offering mental health support, nutritional guidance, and wellbeing resources is no longer just a “nice to have” — it’s become a strategic investment in productivity, engagement, and retention. But many employers still wonder: If we fund these kinds of benefits, do they count as taxable income for employees?

Major changes to company car tax deductions starting in Poland from 2026 Beginning January 2026, Polish rules for deducting the cost of passenger vehicles used for business purposes (tax depreciation) will undergo significant changes. The new regulations, adopted in 2021 yet effective 2026, will introduce stricter limits, shifting the focus from the vehicle’s value to its CO₂ emissions. This marks a major policy shift that will particularly impact businesses purchasing combustion engine vehicles.

More and more entrepreneurs are considering transforming their general partnership (“spółka jawna”) into a limited partnership (“spółka komandytowa”) in Poland. Although both types of entities are subject to Polish CIT, the latter offers certain tax deductions on the partner-level. But could this change be seen as a tax avoidance scheme?